Blog

Info Center

We keep you up-to-date on the latest tax changes and news in the industry.

Naming Your IRA Beneficiary – More Complicated Than You Might Expect

Article Highlights:

How Naming Beneficiaries Impacts Traditional IRA Distributions

The Impact of Naming Your Trust as a Beneficiary

IRA Beneficiary Taxation

The decision concerning whom you wish to designate as the beneficiary of your traditional IRA is critically important. This decision affects:

Who will get what remains in the account after your death, and

How that IRA balance can be paid out to beneficiaries.

What's more, a periodic review of your IRA beneficiaries is vital to ensure that your overall estate planning objectives will be achieved considering changes in the performance of your IRAs and in your personal, financial, and family situation. For example, if your spouse was named as your beneficiary when you first opened the account several years ago and you’ve subsequently divorced, your ex-spouse will remain the beneficiary of your IRA unless you notify your IRA custodian to change the beneficiary designation.

The issue of naming a trust as the beneficiary of an IRA comes up regularly. There is no tax advantage to naming a trust as the IRA beneficiary. Of course, there may be a non-tax-related reason, such as controlling a beneficiary’s access to money; thus, naming a trust rather than an individual or individuals as the beneficiary of an IRA could achieve that goal.

Generally, trusts are drafted so that IRA required minimum distributions (RMDs)will pass through the trust directly to the individual trust beneficiary and, therefore, be taxed at the beneficiary’s income tax rate. However, if the trust does not permit distribution to the beneficiary, then the RMDs will be taxed at the trust level, which has a tax rate of 37% on any taxable income in excess of $15,200 (2024 rate). This high tax rate applies at a much lower income level than for individuals.

Distributions from traditional IRAs are always taxable whether they are paid to you or, upon your death, paid to your beneficiaries. Once you reach age73(years 2023 through 2032),you are required to begin taking distributions from your IRA. If your spouse is under the age of73upon inheritance of your IRA he or she can delay distributions until he or she reaches age73.

The rules are tougher for non-spousal beneficiaries, who generally must begin taking distributions based upon a complicated set of rules. The following details the distribution options from an IRA inherited after 2019 by a non-spousal beneficiary, which includes several categories of beneficiaries.

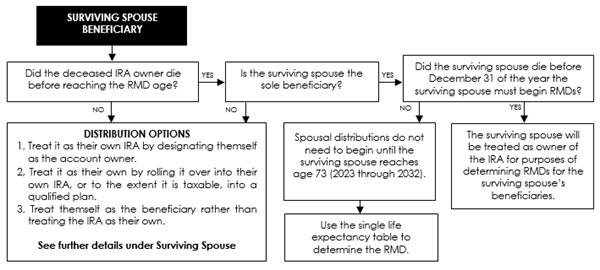

SURVIVING SPOUSE BENEFICIARY

The options available to surviving spouse beneficiaries include:

Treat it as their own IRA by designating themself as the account owner.

Treat it as their own by rolling it over into their own IRA, or to the extent it is taxable, roll it into a:

a. Qualified employer plan (Sec 401(k) plan),

b. Qualified employee annuity plan (Sec 403(a) plan),

c. Tax-sheltered annuity plan (Sec 403(b) plan),

d. Deferred compensation plan of a state or local government (Sec 457 plan), orTreat themself as the beneficiary rather than treating the IRA as their own.

Treating It As Their Own – The surviving spouse will be considered to have chosen to treat the IRA as their own if:

Contributions (including rollovers) are made to the inherited IRA, or

The surviving spouse does not take the required minimum distribution for a year as a beneficiary of the IRA.

The surviving spouse will only be considered to have chosen to treat the IRA as their own if:

The surviving spouse is the sole beneficiary of the IRA, and

The surviving spouse has the unlimited right to withdraw amounts from it.

However, if the surviving spouse receives a distribution from the deceased spouse's IRA, the surviving spouse can roll that distribution over into their own IRA within the usual 60-day time limit for rollovers, provided the distribution isn’t an RMD. This is true even if the surviving spouse is not the sole beneficiary of the deceased spouse's IRA.

Surviving spouse is sole designated beneficiary – If the IRA owner died on or after the RMD required beginning date and the surviving spouse is the sole designated beneficiary, the life expectancy the spouse must use to figure the RMD may change in a future distribution year. This applies where the spouse is older than the deceased owner or the spouse treats the IRA as his or her own.

Special Rules for Sole Surviving Spouse:

Deceased IRA owner died before reaching the RMD starting date

o Spousal distributions do not need to begin until the surviving spouse reaches age 73 (years 2023 through 2032).

o If the surviving spouse dies before December 31 of the year the surviving spouse must begin RMDs, the surviving spouse will be treated as the owner of the IRA for purposes of determining RMDs for the surviving spouse’s beneficiaries.

o Use the Single Life Expectancy table to determine the surviving spouse’s RMD.

OTHER BENEFICIARIES (Except Eligible Designated Beneficiaries)

Can take a lump sum distribution or:

Beneficiaries more than 10 years younger than the decedent are subject to the 10-year rule.

Beneficiaries NOT more than 10 years younger than the decedent may take a lifetime payout.

Ten-Year Rule – The account must be depleted by the end of the year that includes the 10th anniversary of the account owner’s death. If the account owner died on or after their required beginning date (RBD), then the beneficiary must ALSO take annual distributions based their life expectancy and then distribute the balance in the 10th year.

ELIGIBLE DESIGNATED BENEFICIARIES

There is a special category for beneficiaries who are not subject to the rule requiring the account be totally distributed in 10 years (except as noted) and may take lifetime distributions or a lump sum distribution. In addition to a surviving spouse, this category includes:

10 Years Younger than the Account Owner - An individual who is not more than 10 years younger than the account owner (typically a sibling of the decedent but could be someone else).

Disabled or Chronically Ill Individual:

A safe harbor for being considered disabled for this purpose is if the individual is determined to be disabled by the Social Security Administration.

To be eligible the individual must provide to the plan administrator proper documentation of their condition by October 31 of the year following the account owner’s death.

Account Owner’s Minor Child –A minor child is one under the age of 21. These special rules apply to minor children:

Annual payments based on the child’s life expectancy must be taken until the child reaches age 21, using the single life tables.

Once reaching age 21, the child is then subject to the 10-year rule for the balance of the account.

Of course, the beneficiary can always take a lump sum distribution.

Beneficiary Of Account Owner Who Died After December 31, 2019.

Example: Tom died in 2024 at age 74. His 66-year-old brother, Bill, is the beneficiary of his IRA. Bill is an eligible designated beneficiary because he isn’t more than 10 years younger than Tom. Thus, he can take lifetime distributions or a lump sum distribution. If Bill was age 82, the same rule would apply, again because he isn’t more than 10 years younger than Tom.

Example: Jill died in 2024 at age 74. Her 22-year-old grandson, Jack, is the beneficiary of her IRA. Jack is not disabled or chronically ill, and he is more than 10 years younger than Jill, so he is not an eligible designated beneficiary. But Jack is a designated beneficiary. Thus, Jack is subject to the 10-year rule.

To ensure that your IRA will pass to your chosen beneficiary or beneficiaries, be certain that the beneficiary form on file with the custodian of your IRA reflects your current wishes. These forms allow you to designate both primary and alternate individual beneficiaries. If there is no beneficiary form on file, the custodian’s default policy will dictate whether the IRA will go first to a living person or to your estate.

This is a simplified overview of the issues related to naming a beneficiary and the impact on post-death distributions. Uncle Sam wants the tax paid on the distributions, and the rules pertaining to how and when beneficiaries must take taxable distributions are very complicated.

It may be appropriate to consult with this office regarding your particular circumstances before naming beneficiaries.

Want tax & accounting tips and insights?

Sign up for our newsletter.